The continuation of the exemption of purchase tax gives a clear support signal for the development of the new energy automobile industry. The future double-point policy and the continuation of the purchase tax exemption policy will offset the impact from the subsidy declining mechanism.

Applicable to catalogue models

According to the above announcement, the new energy vehicles that are exempt from vehicle purchase tax are managed through the issuance of the Catalogue of New Energy Vehicles Exempt from Vehicle Purchase Tax. New energy vehicles that have been included in the catalogue before December 31, 2017 will continue to be effective in exempting the vehicle purchase tax policy.

Since the beginning of this year, the Ministry of Industry and Information Technology has issued 15 batches of "New Energy Vehicle Model Catalogue Exempt from Vehicle Purchase Tax". According to the announcement, new energy vehicles listed in the Catalogue from January 1, 2018 must also comply with: pure electric vehicles, plug-in (including extended-program) hybrid vehicles, and fuel cell vehicles licensed for sale in China. Meet the technical requirements of new energy automotive products. Through the special inspection of new energy vehicles, the special inspection standards for new energy automobile products are reached. New energy vehicle manufacturers or imported new energy vehicle dealers meet relevant requirements in terms of product quality assurance, product consistency, after-sales service, safety monitoring, and power battery recycling.

The China Automotive Technology and Research Center pointed out that the technical requirements for new energy vehicle products proposed for exemption from purchase tax are generally consistent with the financial subsidy policy for the promotion and application of new energy vehicles in 2017. The technical threshold for individual indicators has been slightly adjusted, but most new energy vehicle products currently meet technical requirements. The products that have entered the duty-free catalogue before 2017 are still valid, avoiding repeated declarations by enterprises.

In addition, the requirements of the exemption of the purchase tax policy for new energy auto companies are consistent with the new energy vehicle production enterprise access regulations and the new energy vehicle promotion and application financial subsidy policy in 2017, and the new product quality assurance and product consistency Sex, after-sales service, safety monitoring, power battery recycling and other aspects have been put forward.

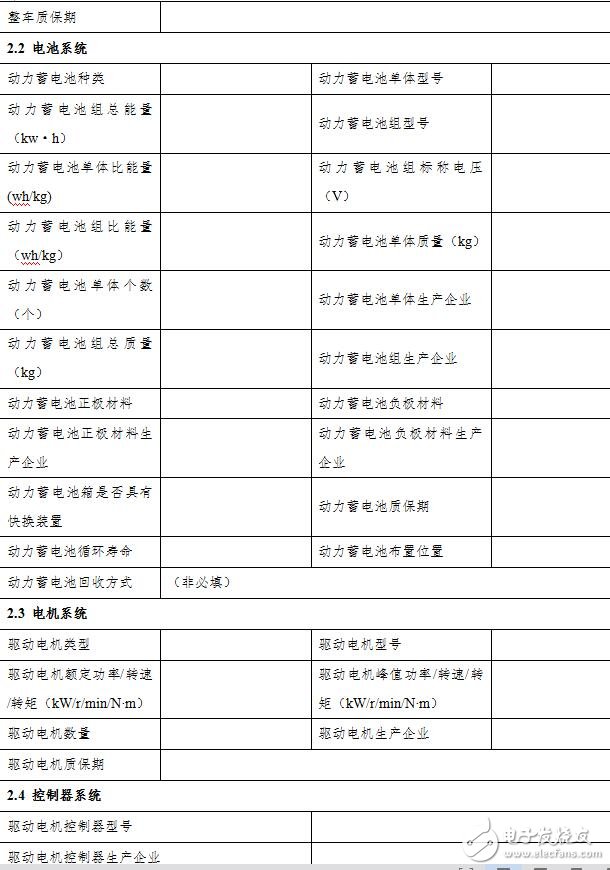

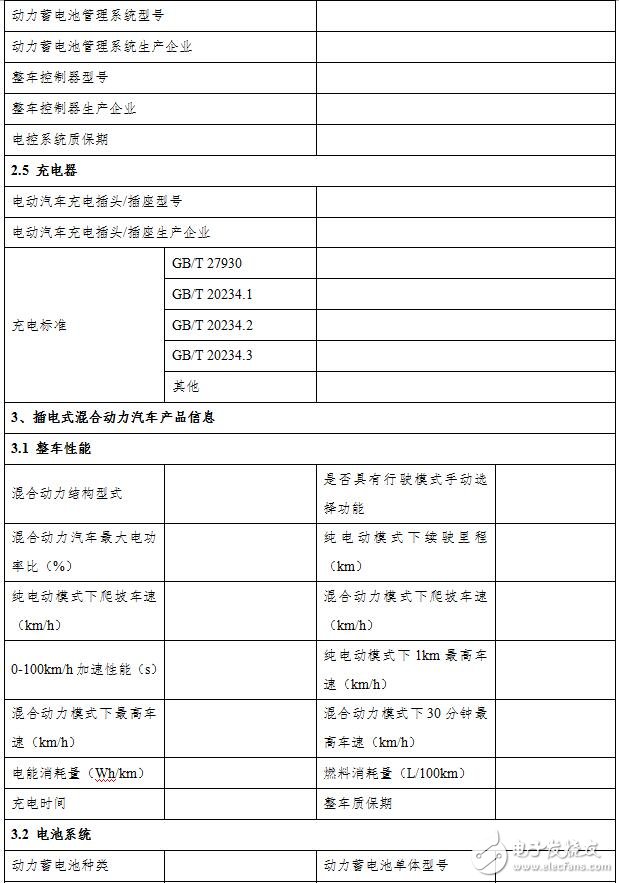

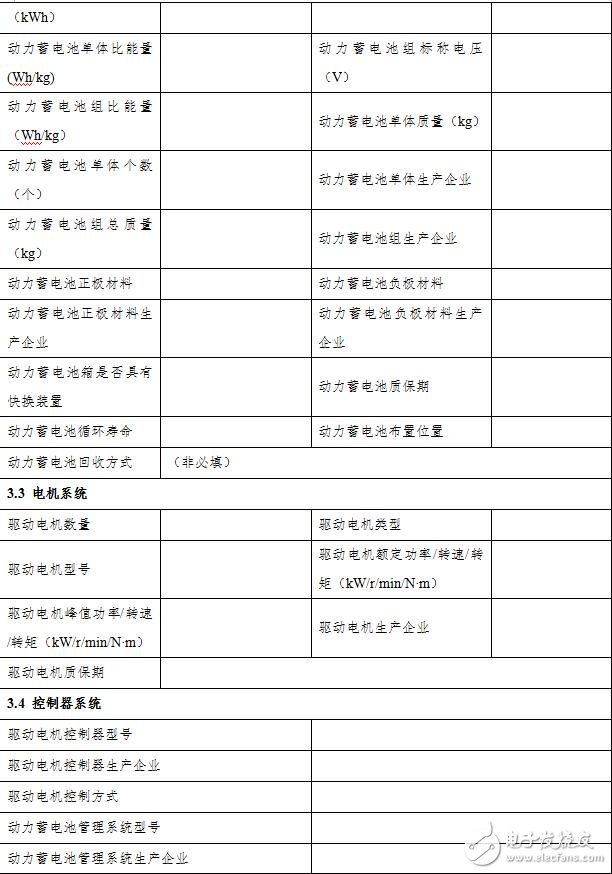

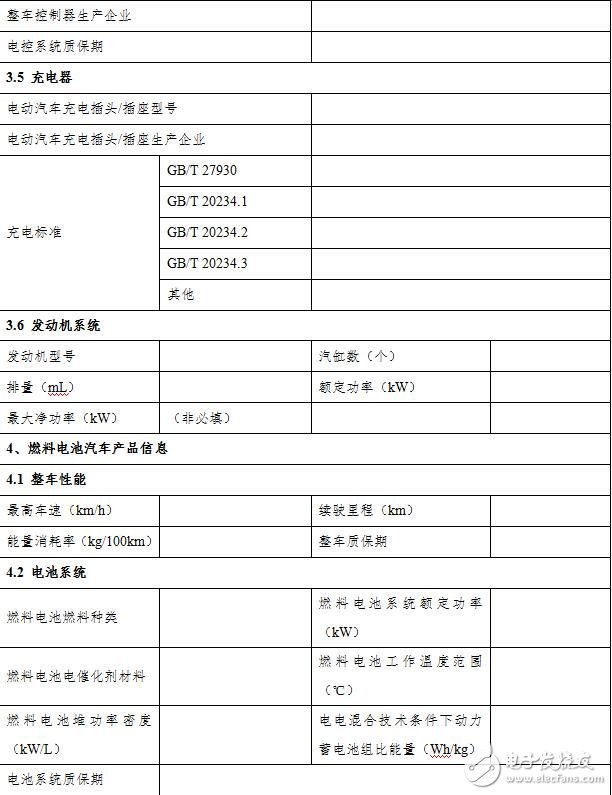

2018 New Energy Vehicle Purchase Tax Catalogue

According to the website of the Ministry of Finance, the Ministry of Finance, the State Administration of Taxation, the Ministry of Industry and Information Technology, and the Ministry of Science and Technology issued the "Announcement on the Exemption of New Energy Vehicle Vehicle Purchase Tax". The announcement stated that from January 1, 2018 to December 2020. On the 31st, the purchase of new energy vehicles was exempted from vehicle purchase tax.

According to the announcement, from January 1, 2018 to December 31, 2020, the purchase of new energy vehicles is exempt from vehicle purchase tax. The new energy vehicles that are exempt from vehicle purchase tax are managed through the issuance of the Catalogue of New Energy Vehicles Exempt from Vehicle Purchase Tax (the “Catalogueâ€). New energy vehicles that have been included in the Catalogue before December 31, 2017 will continue to be effective in exempting the vehicle purchase tax policy.

The announcement states that new energy vehicles listed in the Catalogue from January 1, 2018 must meet the following conditions:

-- Licensed for pure electric vehicles, plug-in (including extended-program) hybrid vehicles, and fuel cell vehicles sold in China.

——In line with the technical requirements of new energy automotive products.

—— Through the special inspection of new energy vehicles, the special inspection standards for new energy automobile products are achieved.

—— New energy vehicle manufacturers or imported new energy vehicle dealers meet relevant requirements in terms of product quality assurance, product consistency, after-sales service, safety monitoring, and power battery recycling.

The announcement emphasizes that enterprises that are not eligible for products and performance indicators, provide other false information, etc., defraud the enterprises listed in the Catalogue, cancel the eligibility for vehicle purchase tax exemption, and comply with relevant laws and regulations. Handle punishment. If there is a safety hazard or a safety accident in the use of the sold product, depending on the nature and severity of the accident, the company shall take measures to stop the production, order the immediate correction, suspend or cancel the eligibility for the exemption of the vehicle purchase tax. Those who engage in the review and examination of the Catalogue application report, and who perform duty-free audits, who have abused their powers, neglect their duties, engage in malpractices, etc., shall be investigated for violations of laws and regulations; if they are suspected of committing crimes, they shall be transferred to the judicial authorities. .

2018 New Energy Vehicle Purchase Tax Announcement Content1. From January 1, 2018 to December 31, 2020, the purchase of new energy vehicles is exempt from vehicle purchase tax.

Second, the new energy vehicles that are exempt from vehicle purchase tax will be managed through the issuance of the Catalogue of New Energy Vehicles Exempt from Vehicle Purchase Tax (hereinafter referred to as the “Catalogueâ€). New energy vehicles that have been included in the Catalogue before December 31, 2017 will continue to be effective in exempting the vehicle purchase tax policy.

3. New energy vehicles listed in the Catalogue from January 1, 2018 shall meet the following conditions:

(1) Pure electric vehicles, plug-in (including extended-program) hybrid vehicles and fuel cell vehicles licensed for sale in China.

(2) Comply with the technical requirements of new energy automobile products.

(3) To meet the special inspection standards for new energy automobile products through special inspection of new energy vehicles.

(4) New energy vehicle manufacturers or imported new energy vehicle dealers (hereinafter referred to as enterprises) meet relevant requirements in terms of product quality assurance, product consistency, after-sales service, safety monitoring, and power battery recycling.

The Ministry of Finance, the State Administration of Taxation, the Ministry of Industry and Information Technology, and the Ministry of Science and Technology will adjust the conditions of new energy vehicles listed in the Catalogue in a timely manner in accordance with the development of new energy vehicle standard systems, technological advances, and vehicle models.

4. The enterprise shall submit a “Application†report to the Ministry of Industry and Information Technology and be responsible for the authenticity of the submitted materials and the quality of the products. The Ministry of Industry and Information Technology will organize technical experts with the State Administration of Taxation to conduct a review. The models that have passed the review are listed in the Catalogue and issued by the Ministry of Industry and Information Technology and the State Administration of Taxation.

5. For new energy vehicles listed in the Catalogue, when the enterprise uploads the information of the vehicle's complete vehicle certificate, it is marked with “Yes†in the field “Whether it is included in the catalogue of new energy vehicle models exempt from vehicle purchase tax†( That is, tax-free identification). The Ministry of Industry and Information Technology will review the tax exemption mark in the vehicle certificate certificate issued by the enterprise, and transmit the information passed the audit to the State Administration of Taxation. The tax authorities handle the tax exemption procedures according to the tax exemption mark and the unified sales invoice (or valid certificate) of the motor vehicle after the review by the Ministry of Industry and Information Technology.

6. Enterprises that do not conform to the product and the declared materials, fail to meet the requirements of the product performance indicators, provide other false information, etc., defraud the enterprises listed in the Catalogue, and cancel the eligibility for the exemption of vehicle purchase tax, and deal with them in accordance with relevant laws and regulations. Punishment. If there is a safety hazard or a safety accident in the use of the sold product, depending on the nature and severity of the accident, the company shall take measures to stop the production, order the immediate correction, suspend or cancel the eligibility for the exemption of the vehicle purchase tax.

7. In the case of staff members who are engaged in the review and examination of the Catalogue application report and who perform the duty-free audit, if they have abused their powers, neglect their duties, engage in malpractices, etc., they shall be in accordance with the Civil Service Law, the Administrative Supervision Law and other relevant countries. It is stipulated that the corresponding responsibility shall be investigated; if it is suspected of committing a crime, it shall be transferred to the judicial organ for handling.

SHENZHEN CHONDEKUAI TECHNOLOGY CO.LTD , https://www.szsiheyi.com